Spain has long been a top destination for elite international talent, particularly in professional sports. This influx creates the need for effective tax residency strategies. Spain’s evolving tax incentives for non-residents, commonly known as the ‘Beckham Law’ and the ‘Mbappe new regime’ are key tools for managing taxation. Unit-linked insurance products offer powerful synergies for wealth preservation and creation under these laws.

What is the Beckham Law?

Originally enacted in 2005 to attract international talent (particularly in football), the Beckham Law refers to Spain’s special tax regime for inbound workers (Ley 35/2006, modified by RD 687/2005):

- Applicable to expatriates who become Spanish tax residents.

- Allows taxation only on Spanish-sourced income (for 6 years), excluding foreign source income.

- Taxpayers are taxed at a flat rate of 24 per cent on Spanish employment income up to 600 000 EUR (47 per cent on the excess).

- Taxation of Spanish-sourced financial income only.

While the law was initially popular among athletes, it was curtailed in 2010 to exclude professional sportspeople. However, professionals in other fields still benefit.

What is the Mbappé Law?

It refers to a Madrid regional tax incentive (Law 4/2024), which was named after Kylian Mbappé since it coincided with his move to Real Madrid. It enables new foreign residents of Madrid who have not lived in Spain for the past five years to claim a 20% tax credit, which can be offset against the regional portion of their personal income tax (IRPF). The amount of the tax credit is based on the investment in qualifying financial assets (such as Madrid-listed or unlisted equities and bonds).

Key eligibility and conditions include:

- The person must not have been a tax resident in Spain in the previous five years.

- He must become and remain a tax resident in Madrid during the mandatory investment period of six years.

- Investments must be in financial assets, not real estate, and not in companies based in tax havens.

- Individual (and close family) ownership must remain below 40%, with no executive roles in the invested company.

The main differences between the two laws

| Beckham law | Mbappé law | |

| Beneficiaries | Designed for employees, especially high-level executives who have been

relocated to Spain, but not professional athletes. | Targeted at large investors moving their tax residence to Madrid,

including professional athletes. |

| Geographic scope | Applies throughout Spain (mainland, islands, Ceuta & Melilla). | Only applies to those residing in the Community of Madrid. |

| Residency requirements |

|

|

| Type of tax benefit |

|

|

How can unit-linked insurance help?

Unit-linked life insurance contracts are hybrid products that combine investment and insurance. They are widely used for their cross-border advantages and for wealth planning under EU law and local regimes.

Benefits of unit-linked products for Spanish tax residents:

- Tax deferral: Any capital gains or financial income within a unit-linked policy grow tax-free until withdrawals are made.

- Inheritance and succession planning: Policies can be set up to name specific beneficiaries and bypass probate.

- Wealth structuring and transfer solutions for inbound workers:

- Invest in a diversified portfolio of assets from Spanish and foreign sources in a compliant unit-linked structure.

- Benefit from income tax deferral until any withdrawal is made, even once the special regime expires.

- Use the policy to repatriate global income after the 6-year exemption period.

- Portability across EU jurisdictions: When issued under the EU Freedom of Services (FoS) regime, these products are portable, which is particularly useful for mobile professionals.

- No exit tax is applicable when leaving Spain.

Putting it all together: A case study

Scenario: A financial trading professional relocates from the UK to Spain in 2025 under the Beckham Law. He earns 5 million euros per year from his salary, including bonuses, and 2 million euros from income generated from financial assets held abroad.

Under the Beckham Law: Only his Spanish income is taxable, at a flat rate of 24% on salary income up to €600 000 and 47% on anything above that, while foreign income is exempt.

Solution: Invest a portion of the untaxed global earnings in our Life Asset Portfolio, which is designed as a Private Placement Life Insurance (PPLI) product.

Result: There is no current taxation on investment returns, and the policy provides long-term capital growth, high death coverage and flexible withdrawal planning once the six-year regime ends.

As Spain modernises its tax landscape for international professionals, this could represent a good alternative to the UK, given that the favourable tax regime for non-habitual residents (RNH) ends in 2025.

Understanding the interplay between special tax regimes and compliant wealth structures is therefore essential.

For those eligible under the Beckham or Mbappé laws, unit-linked insurance solutions are among the most efficient, compliant and flexible tools available.

Swiss Life Generations-a highly efficient wealth structuring solution

As mentioned in our Spring newsletter, Swiss Life Generations is a unique solution that offers optimum protection and flexibility by combining the advantages of a life insurance policy with ultra-high life cover.

Some practical examples are provided here on how Swiss Life Generations can be a highly effective solution for wealth structuring.

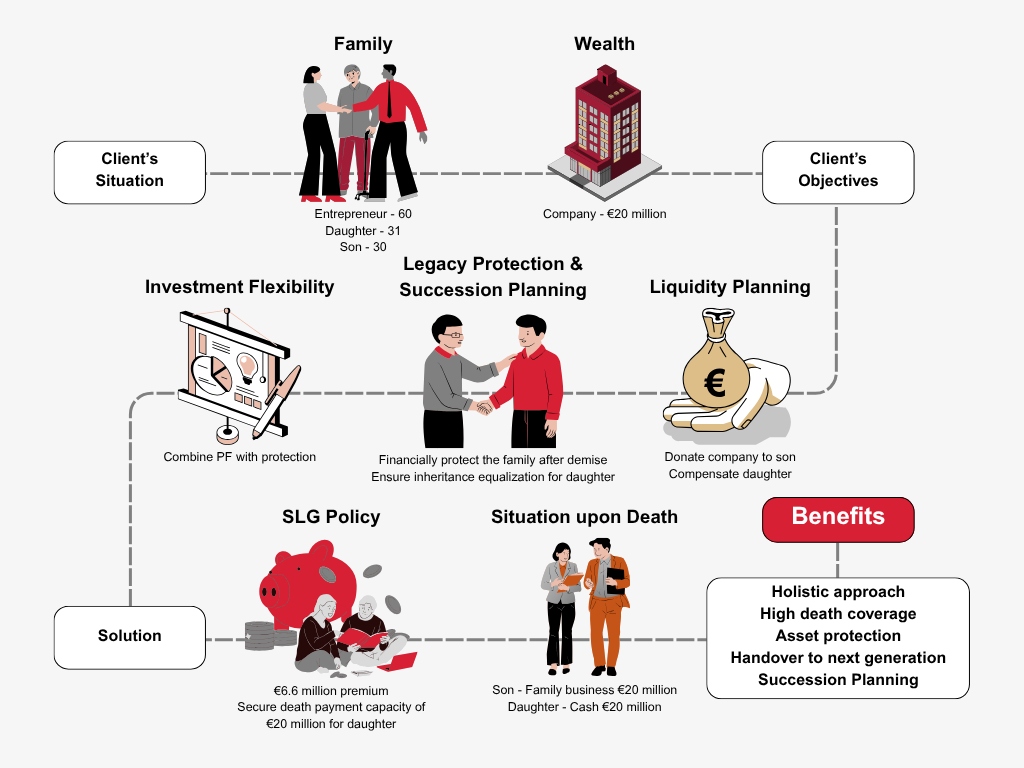

How can I ensure inheritance equalisation?

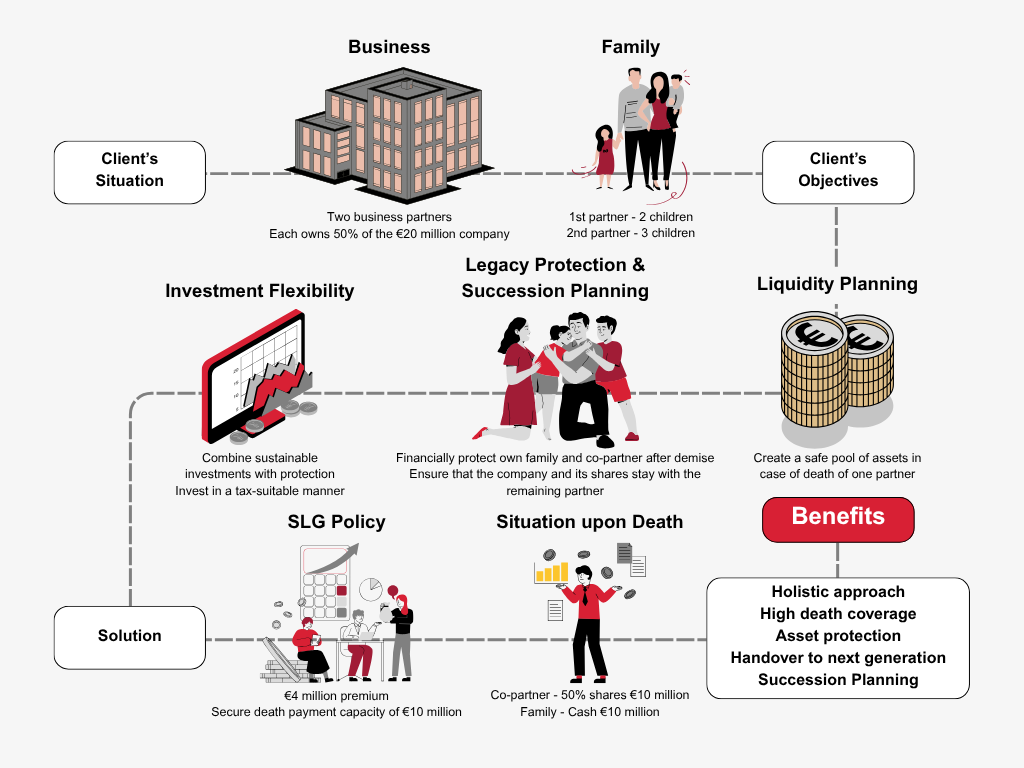

How can I insure my company's future?

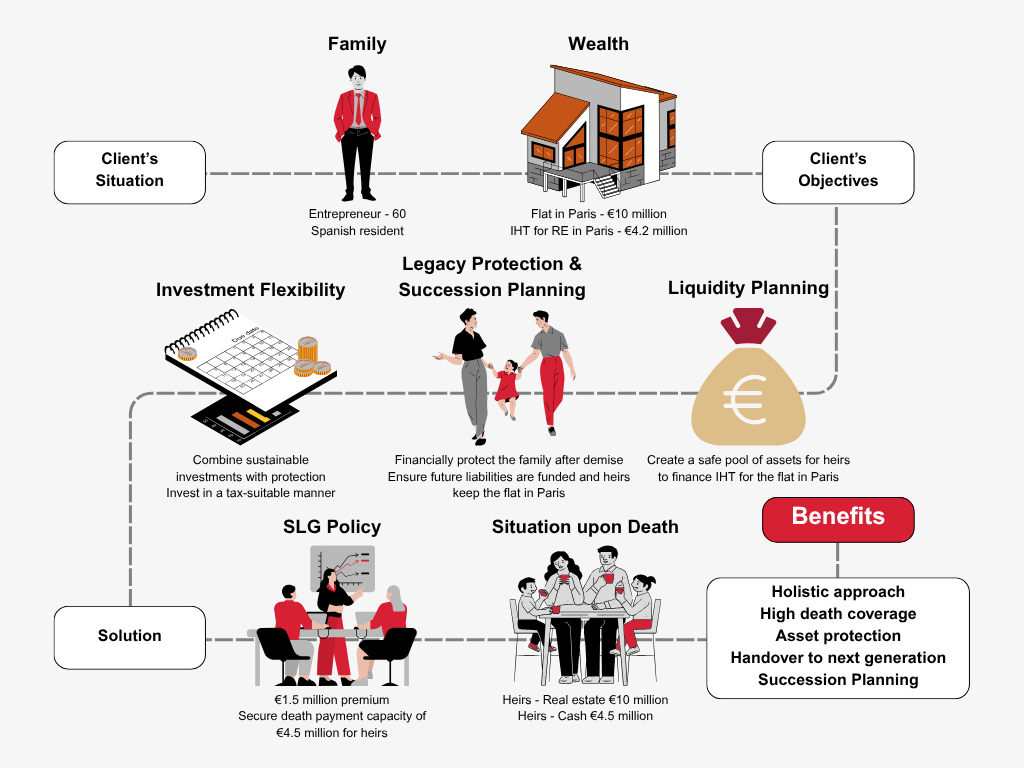

How can I finance inheritance tax on real estate abroad?

*These are practical examples, for an offer please contact us.

Contact us

Our teams are at your disposal to find out how to integrate this solution into your offer or to support you in optimising wealth solutions for your clients.

More information on Swiss Life Generations

With our bespoke wealth management solution grow your financial assets while simultaneously protecting your loved ones.